Wall Street closes at a record for the first time since end of January

Introduction & Market Context

CVC Corp (BVMF:CVCB3) presented its fourth quarter and full-year 2025 results on March 19, 2026, showcasing significant profitability improvements and operational expansion despite missing quarterly revenue expectations. The Brazilian travel company reported consolidated EBITDA growth of 18% year-over-year while expanding its physical footprint by 196 stores to reach 1,646 locations across its markets.

The company’s stock rose 1.04% to R$1.93 following the presentation, suggesting investor confidence in the strategic direction despite fourth quarter revenue of R$362.1 million falling short of the R$394.24 million forecast. According to InvestingPro analysis, the stock appears undervalued at current levels, with the company maintaining an impressive 97% gross profit margin.

Financial Performance Highlights

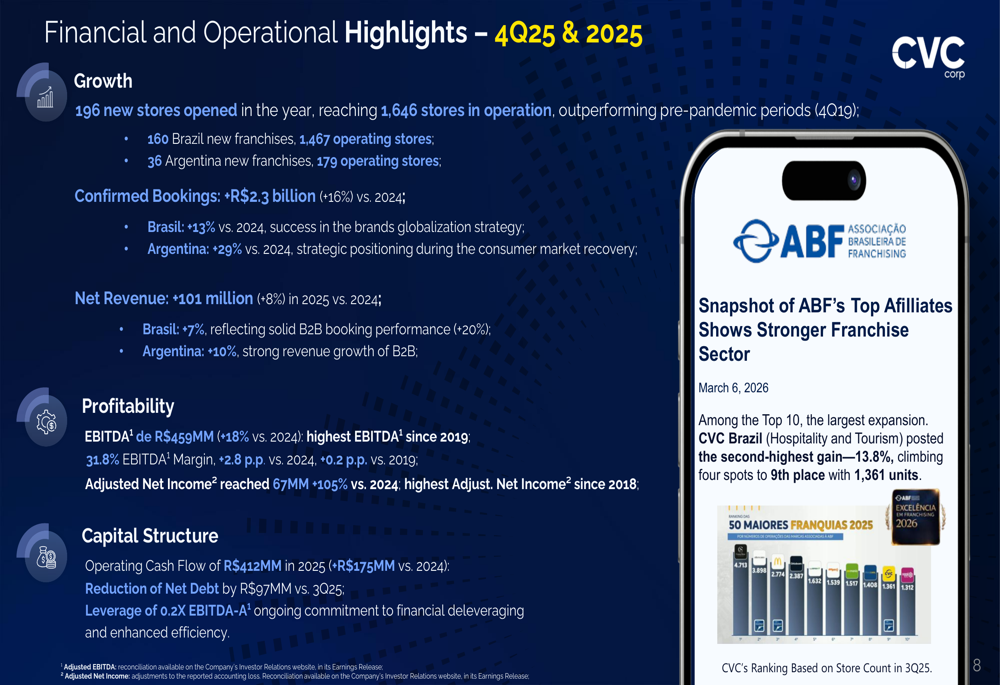

As shown in the following comprehensive overview of CVC’s 2025 achievements, the company demonstrated strong momentum across multiple operational and financial metrics.

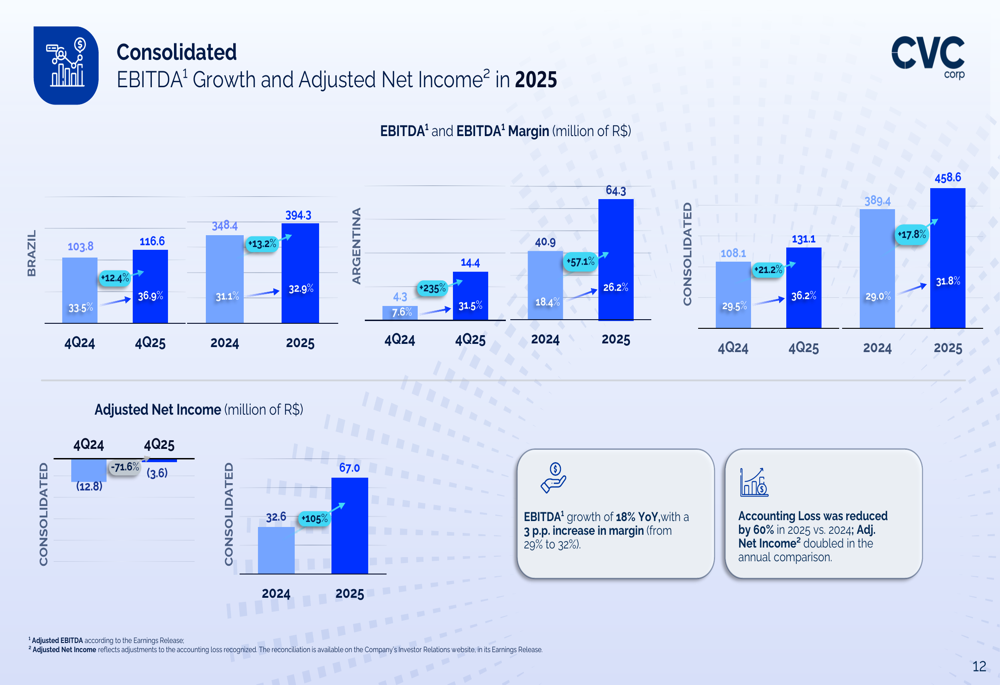

CVC’s full-year 2025 performance reflected robust growth in core business metrics. Confirmed bookings reached R$2.3 billion, representing 16% growth versus 2024, with Brazil contributing 13% growth and Argentina delivering an impressive 29% increase. Net revenue for the full year totaled R$1,442.9 million, up 7.6% year-over-year, though the fourth quarter showed a modest 1.2% decline to R$362.1 million.

The company’s profitability metrics told a more compelling story. EBITDA reached R$459 million for the full year, an 18% improvement over 2024, with margins expanding to 31.8%. Adjusted net income more than doubled to R$67 million, up 105% from the previous year’s R$32.6 million.

Brazil Operations Drive Core Growth

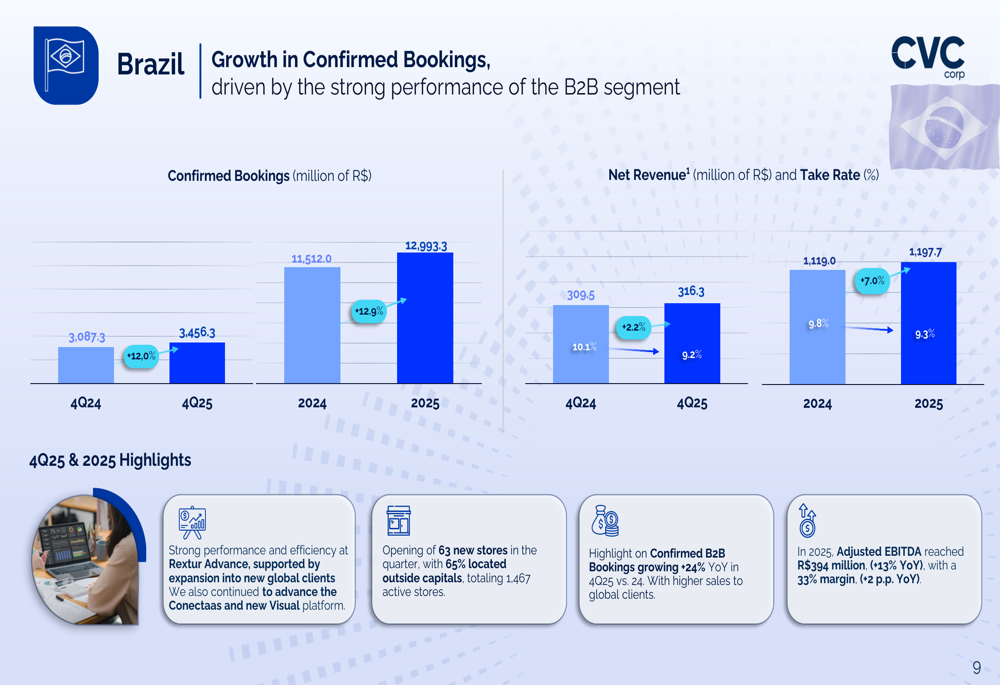

The Brazilian market, representing CVC’s largest revenue contributor, demonstrated steady expansion throughout 2025. As illustrated in the following breakdown of the Brazil segment’s performance, confirmed bookings and revenue growth remained positive despite moderating take rates.

Brazil’s confirmed bookings climbed 12.9% for the full year to R$12,993.3 million, with fourth quarter bookings reaching R$3,456.3 million, up 12.0% year-over-year. Net revenue in Brazil grew 7.0% annually to R$1,197.7 million, though fourth quarter growth moderated to 2.2%. The Brazil segment achieved a 33% EBITDA margin in the fourth quarter, representing a 2 percentage point improvement year-over-year.

Strategic initiatives in Brazil showed tangible progress. The following chart demonstrates how CVC’s focus on preferred hotel partnerships, exclusive products, and global client relationships evolved throughout 2025.

Preferred hotel participation surged from 64.3% in the fourth quarter of 2024 to 79.1% by the end of 2025, reflecting strengthened supplier relationships. Global clients’ share in B2B sales expanded dramatically from just 0.7% to 10.1% over the same period, indicating successful diversification of the customer base. Meanwhile, the company diversified payment methods, with credit card usage declining from 68% to 60% as alternative payment options gained traction.

Argentina Benefits from Economic Recovery

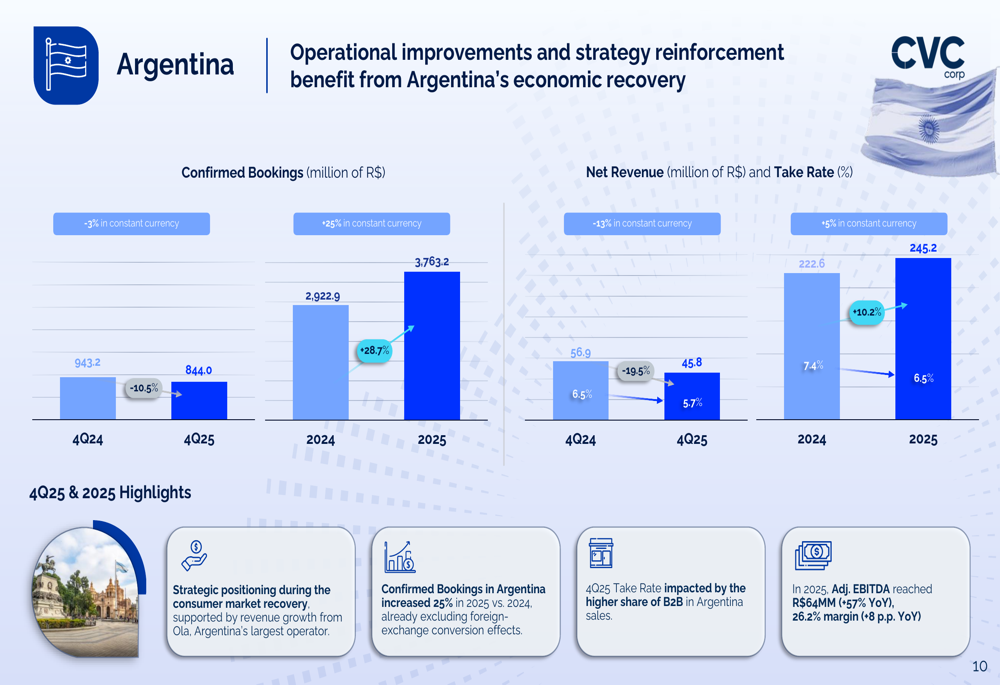

CVC’s Argentine operations capitalized on the country’s economic stabilization, delivering substantial margin improvements. The following regional breakdown illustrates Argentina’s operational turnaround and strategic positioning.

Argentina posted confirmed bookings of R$3,763.2 million for 2025, up 28.7% year-over-year, despite fourth quarter bookings declining 10.5% to R$844.0 million amid seasonal factors. Net revenue reached R$245.2 million for the full year, representing 10.2% growth, though the fourth quarter saw a 19.5% decline to R$45.8 million.

The standout performance came in profitability metrics, with Argentina’s fourth quarter EBITDA margin reaching 26.2%, an 8 percentage point improvement year-over-year. This margin expansion reflected operational efficiencies and the benefits of Argentina’s economic recovery.

Strategic Transformation Underway

CVC outlined five strategic pillars guiding its transformation, as detailed in the company’s strategic framework presentation.

The company’s strategic focus encompasses customer centricity, digital transformation, profitability expansion, globalization, and cultural transformation. Under CEO Fábio Mader’s leadership, CVC implemented a new organizational structure designed to accelerate these initiatives.

The leadership team structure reflects the strategic priorities, with dedicated verticals for digital operations, client experience, and international expansion. As shown in the following organizational chart, CVC appointed experienced executives to key positions while creating new roles to drive transformation.

Notable appointments include Bob Rossato leading digital initiatives with 29 years of experience, Diego Garcia overseeing Argentine operations with 36 years in the industry, and Felipe Gomes managing finance, legal, strategy and investor relations with 12 years of experience.

Margin Expansion and Efficiency Gains

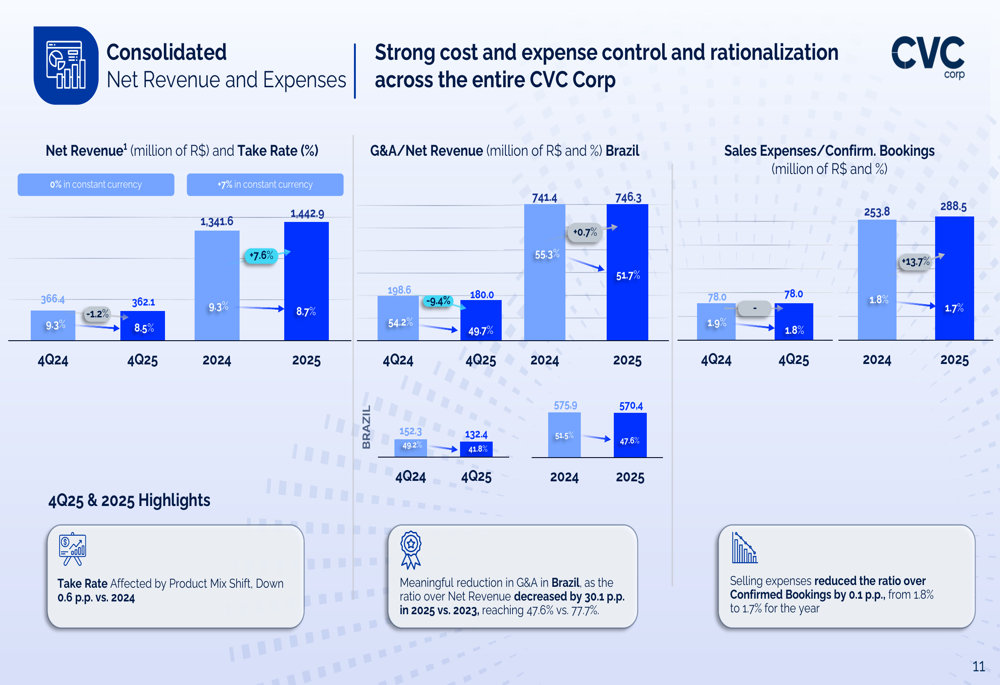

The company’s focus on profitability yielded measurable improvements in operational efficiency. As demonstrated in the following consolidated expense analysis, CVC achieved better cost management while maintaining revenue growth.

General and administrative expenses as a percentage of net revenue improved to 49.7% for the full year 2025, down 9.4 percentage points from 2024, though fourth quarter G&A/revenue ratio increased slightly to 51.7%. Sales expenses relative to confirmed bookings remained disciplined at 1.7% for the year.

The profitability improvements translated into strong EBITDA performance across both operating segments. The following detailed breakdown shows how Brazil and Argentina contributed to consolidated EBITDA growth.

Brazil generated R$116.6 million in EBITDA for the fourth quarter, up 12.4% year-over-year, while Argentina contributed R$7.6 million, representing a 235% surge. For the full year, consolidated EBITDA reached R$458.6 million, an 17.8% increase, with margins expanding to 31.8% from 31.1% in the prior year.

Capital Structure Strengthens

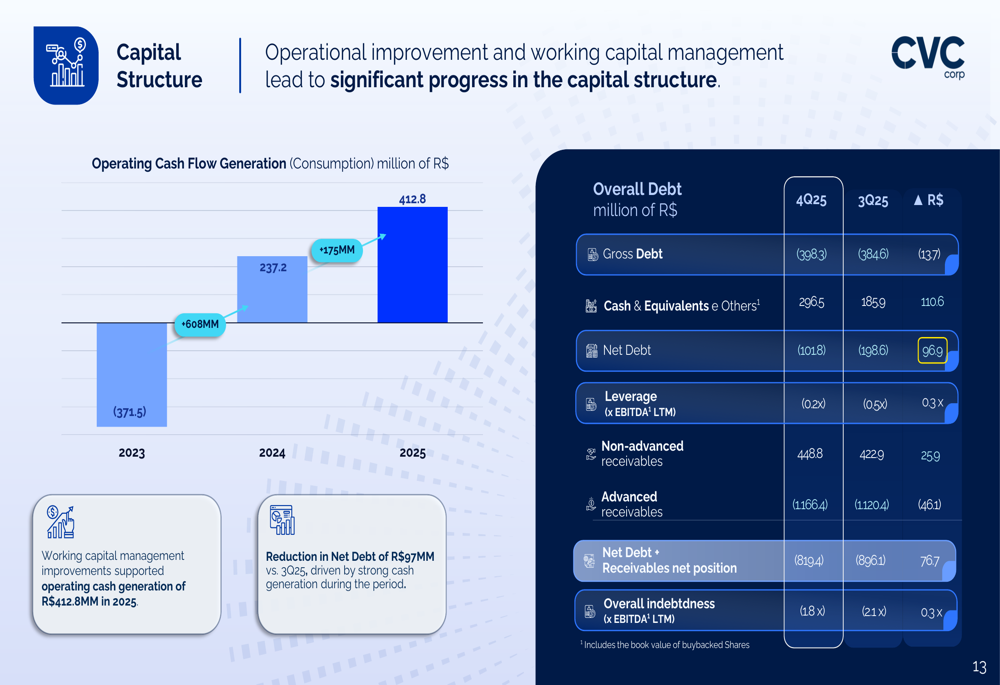

CVC made significant progress in deleveraging and improving financial flexibility during 2025. The following capital structure overview illustrates the company’s strengthened balance sheet position.

Operating cash flow generation reached R$412.8 million for 2025, a 74% increase from the previous year’s R$237 million. This robust cash generation enabled the company to reduce net debt by R$97 million versus the third quarter of 2025, with net debt declining to R$101.8 million.

The company’s leverage ratio improved to negative 0.2x EBITDA, while overall indebtedness including receivables reached negative 1.8x EBITDA. Gross debt stood at R$398.3 million, offset by cash and equivalents of R$296.5 million. The company maintained R$448.8 million in non-advanced receivables against R$1,166.4 million in advanced receivables.

Outlook and Analyst Perspectives

Despite the fourth quarter revenue miss, market reaction remained positive with the stock gaining 1.04% following the presentation. InvestingPro analysis suggests the stock appears undervalued at current levels, with a market capitalization of $193 million and strong gross profit margins of 97%.

However, InvestingPro Tips highlight important considerations for investors, noting that analysts do not anticipate profitability in the current year and that the stock trades with high price volatility. The company’s financial health scores as "GOOD" overall on InvestingPro’s comprehensive rating system.

CEO Fabio Mader emphasized the company’s strategic focus, stating, "Our commitment to innovation and operational excellence has positioned us well for sustainable growth." CFO Felipe Gomes highlighted the importance of deleveraging efforts, noting, "Our improved leverage ratio reflects our dedication to financial health and strategic growth."

For 2026, CVC provided optimistic guidance projecting continued expansion of its product offerings and enhancement of digital capabilities to drive future growth. The company’s expansion to 1,646 stores, combined with improving digital penetration and global client relationships, positions CVC to capitalize on Brazil’s travel market recovery while benefiting from Argentina’s economic stabilization.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.